By Joseph Ciccolini, content marketing associate, Young & Associates

Marketing often takes a back seat at financial institutions. While many recognize its potential to drive new accounts and attract customers, institutions frequently underemphasize its role as a revenue-generating function. In many cases, the solution already exists but needs to be positioned more effectively: cross-selling, particularly through the “gateway” product that establishes a primary relationship.

For financial institutions, profitability is not just about volume growth but also depth in relationships. Checking accounts provide a natural starting point for building stronger customer engagement, increasing retention, and expanding cross-sell potential.

A 2025 Jack Henry Strategy Benchmark identified top priorities for bank and credit union CEOs, including improving efficiency, driving deposit and loan growth, acquiring new accountholders, and expanding solutions for small and medium-sized businesses. Checking account acquisition directly supports each of these priorities by establishing a primary customer relationship that enables deeper engagement, stronger retention, and increased opportunities for cross-selling.

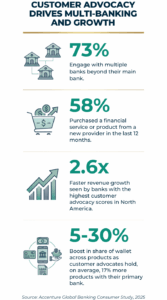

Consumers typically define their primary financial institution as the one where they hold their primary checking account. That account serves as the gateway to cross-selling opportunities and deeper customer relationships. Primary financial institution relationships are remarkably stable, with customers staying with the bank for an average of eight to 10 years and using five to six products and services per household. Without it, customers are less likely to view the institution as their primary provider. Instead, the relationship resembles the financial equivalent of a secondary streaming service — used occasionally, but not the go-to.

What strategies can institutions use to encourage customers to open a checking account and become primary accountholders? One effective approach is a drip campaign.

What are drip campaigns?

Drip campaigns are a form of email marketing that deliver targeted messages over time to encourage engagement and keep your institution top of mind with customers and prospects. By providing relevant, valuable information, these campaigns guide customers toward action through continuous communication. This approach helps institutions nurture leads and build strong, long-term relationships.

In this context, a drip campaign supports the goal of securing the “gateway” cross-sell in the form of a checking account. Once a customer opens a checking account, the likelihood of becoming a primary accountholder increases significantly, along with opportunities to expand the relationship.

Cross-selling differs from upselling by focusing on complementary products that enhance the customer relationship and increase overall value. The checking account serves as the entry point for this strategy. Once established, institutions can introduce additional products — such as debit cards or certificates of deposit — in a way that aligns with customer needs and behaviors.

Why drip campaigns can outperform cash incentives

Some institutions may already rely on cash incentives to encourage checking account acquisition. However, a 2025 ProSight industry outlook found that only 27 percent of consumers who recently switched institutions cited a cash incentive as the primary reason. Instead, institutions should identify customer needs, understand the challenges they can solve, and promote those solutions effectively.

Drip campaigns play a key role in this strategy by delivering relevant, timely messaging directly to customers. These campaigns help move prospects from consideration to conversion while setting the stage for meaningful interactions.

Gallup’s 2021 retail banking study found that high-quality conversations significantly improve sales conversion rates. When customers initiate the conversation, conversions are 1.6 times more likely compared with low-quality interactions. When employees initiate high-quality conversations, conversions are 4.2 times more likely. Drip campaigns can help prompt these conversations by engaging customers before direct interaction occurs.

Conclusion

Financial institutions should treat checking account acquisition as a critical step in attracting and retaining customers. According to the J.D. Power 2026 U.S. Retail Banking Satisfaction Study, key engagement metrics are beginning to decline as customers increasingly open accounts with multiple institutions. This shift creates a clear opportunity to attract new customers and strengthen relationships through effective cross-selling.

All of this can start with a checking account. Financial institutions should move beyond traditional go-to-market approaches and adopt a marketing-led strategy that prioritizes engagement, not just acquisition. By using tools like drip campaigns to convert and deepen relationships, institutions can turn checking accounts into a foundation for long-term growth and differentiation.