By Michael Gerbick; president, Young & Associates

Last year the FDIC filed a lawsuit against 17 former executives and board directors of Silicon Valley Bank (SVB) for alleged negligence and breach of fiduciary responsibility, which led to the collapse in March 2023. We all know what happened with SVB and the other institutions that failed around this time in 2023.

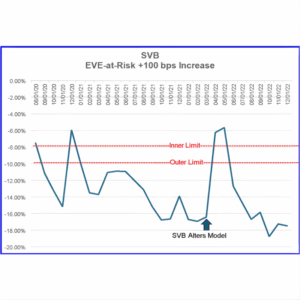

I reviewed the FDIC’s lawsuit again this year, given the current rate environment. A particular section of the lawsuit sticks out to me on assumption adjustments extending the average life of deposits and resulting EVE at risk after the adjustment.

“As reported in a May 24, 2022, presentation to the Asset Liability Management Committee, SVB’s officers implemented this plan by changing the curtailment assumption from 5.5 to 12 years…. Without any valid justification for the change.”

Why you need to justify your model assumptions

Many ALM and Liquidity models continue to improve with the integration of institutions’ core systems and considering additional details of your assets and liabilities. The institution’s model assumptions and governance remain critical to the reliability of the model’s forecasts. Model assumptions should be supported, reasonable, and appropriate. Strong governance also includes documentation of model development and validation that is sufficiently detailed to allow parties unfamiliar with a model to understand how the model operates, as well as its limitations and key assumptions. Assumptions reflect our prediction of customer behavior. Because behaviors can change quickly, institutions should review assumptions regularly. A method to identify risk is to stress these assumptions.

Specific to liquidity modeling and deposits, I want to dive into a few assumptions for stress testing. As we have exited the pandemic environment of zero rates and the rapid hike of 550 bps, we learned a considerable amount regarding customer behaviors. First and foremost, assumptions that modelers applied to historic trends may not translate the same way today. The rate increases and available technology created an environment where savvier depositors now demand a higher rate of return on what institutions once viewed as less price-sensitive core deposit categories.

Regarding liquidity, institutions had to provide more competitive pricing on their non-maturities, different products (perhaps CDs with higher rates of return), or experience runoff and leverage wholesale funding at a higher rate than they were accustomed to with the core deposit. Historic customer behavior trends of the past are a key component, but not the only component for developing assumptions to the models.

That rate environment is in the past, but the savvy customer remains in today’s environment. The deposit composition at many institutions changed. Customers are comfortable leveraging technology to move money in and out of an institution to a more favorable situation, no longer assumed to be as loyal as they once were. It is not a conclusion that behaviors experienced in 2020-2023 will remain, but it is prudent to consider the technologies available today and this history in how institutions establish model assumptions and stress testing. The stress tests should reflect the specific institution, risk profile, and hypothetical scenarios.

A set of valuable stress levers for consideration are:

A set of valuable stress levers for consideration are:

- Runoff by deposit type and customer (if available). Historic trends may be helpful for a baseline, but the rate environments these trends may be based on could be from 5+ years ago.

- Regulators encourage institutions to review and stress the rate of runoff. More competitors exist today in local markets with online banks, fintech and brokerages. Consider various product types and how customers may react under various stresses. Scenarios may include only retaining a percentage of CD balances, Money Markets runoff may be different than Savings accounts or Large Uninsured Deposits. If the ability to review customer level behavior focused on movement between accounts, the institution may be able to incorporate insights into the overall stress tests. Strategic plans may follow the insights gained from the stress tests.

- Leverage the customer level behavior knowledge for strategies to provide more valuable products and services, consider digital marketing efforts (and partners), consider total relationship (deposits) when a new lending relationship develops.

- Access to Wholesale Funding.

- Consider haircuts on availability or inability to access line of credits from providers. Consider stress scenarios in which management cannot access brokered deposits they rely on to offset core deposit runoff.

- Some institutions have agreements in place but do not regularly leverage wholesale funding. Testing these lines (at least) annually helps ensure personnel know how to quickly access the funds, minimizing risk of disruption when it comes time to leverage them.

The lawsuit above accuses SVB of adjusting its assumptions without justification. I encourage you to review and stress yours. Customer behaviors can change swiftly. Reviewing what customers are doing today at your institution and thinking through the impact those behaviors may have on your liquidity if they remain stable and what risks appear should those behaviors become more severe could provide you with useful information you can use today to protect your bank tomorrow.

I’m interested in how your institution establish assumptions and stress test scenarios. I would welcome any conversation on this topic. You can email me at mgerbick@younginc.com with any thoughts!

Reviewing and stress‑testing your assumptions is key to managing liquidity risk. Young & Associates can help your institution strengthen its liquidity framework and meet evolving regulatory expectations. If we can assist your institution in these areas, contact us today.