Analyzing the OCC’s Spring 2026 Semiannual Risk Perspective for community bankers

The OCC’s Spring 2026 Semiannual Risk Perspective gives community financial institutions a strategic view of the most significant risks affecting the banking industry. Using the National Risk Committee’s latest findings, the report helps bank leaders evaluate institutional strength, identify emerging threats, and align risk management strategies with evolving federal regulatory expectations. This article examines the key insights and banking industry trends highlighted in the Spring 2026 report.

As the banking industry moves through the spring of 2026, U.S. financial institutions face a market defined by speed, volatility, and structural change. Strong earnings and high liquidity continue to support the system, but rising geopolitical tensions, AI-driven fraud, and mounting commercial real estate refinancing pressure are forcing banks to rethink traditional risk management strategies.

The banking system enters 2026 from a position of strength

The 2026 macroeconomic outlook and structural headwinds

- Geopolitical Risk: The conflict in the Middle East is a primary concern, with the potential to disrupt global energy flows (particularly through the Strait of Hormuz) and fuel inflation.

- Credit Headwinds: While aggregate credit risk is manageable, specific segments — including commercial real estate (CRE), private credit markets, and consumer credit for lower-score borrowers — require ongoing monitoring.

- Operational Threats: Cybersecurity remains an elevated risk, driven by sophisticated foreign state-sponsored actors and the emergence of advanced AI tools that enhance the speed and scale of attacks.

- Regulatory Evolution: The OCC continues to implement the GENIUS Act regarding stablecoins and is working to tailor compliance requirements to reduce the burden on community banks while addressing increased sanctions and money laundering risks.

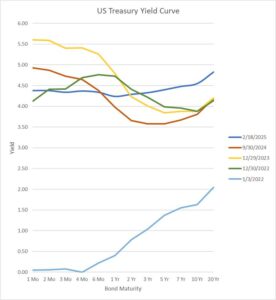

U.S. economy continues growing despite inflation risks

Labor and inflation

- Labor Market: Unemployment remained low at 4.3 percent as of March 2026. While payroll gains were strong in the first half of 2025, they reversed in the second half, leading to a characterized state of “employer caution” in early 2026. Wage growth eased to 3.4 percent by the end of 2025.

- Inflation: Core inflation started 2026 at 3.1 percent, remaining above the Federal Reserve’s 2 percent target. Stickiness in service-sector inflation and high shelter costs persist.

- Monetary Policy: After holding rates steady in early 2025, the Federal Reserve implemented three rate cuts in the second half of that year.

2026–2027 economic projections

Significant economic risks

- Strait of Hormuz: Sustained closure could drive higher energy costs, reducing consumer purchasing power and increasing business production expenses.

- Interest Rate Expectations: Market participants have adjusted expectations downward; the April forecast anticipates only one rate cut in 2026, while financial market pricing suggests even that may not occur.

Bank performance analysis

Financial trends (2024–2025)

|

Metric

|

System Total (2025)

|

System % Change

|

Community Banks (2025)

|

Community % Change

|

|---|---|---|---|---|

|

Net Interest Income

|

$493.9 Billion

|

+3.7%

|

$34.4 Billion

|

+12.2%

|

|

Noninterest Income

|

$249.6 Billion

|

+11.0%

|

$11.0 Billion

|

+7.1%

|

|

Net Income

|

$199.2 Billion

|

+8.8%

|

$12.5 Billion

|

+21.6%

|

|

Total Loan Balances

|

—

|

+6.0%

|

—

|

+5.0%

|

Key financial risks

Credit risk

- CRE: Office properties still face high vacancy rates, though net absorption turned positive in late 2025. Refinancing risk is a major concern as loans originated in low-interest environments mature. Conversely, retail remains a “bright spot” with low vacancy rates.

- Private Credit: While generally performing well, there are signs of weakening in some sectors. The use of “paid-in-kind” (PIK) mechanisms and debt restructurings may be masking underlying credit deterioration.

- Consumer Credit: Delinquencies have increased among borrowers with lower credit scores, though supervised banks have manageable exposure to these higher-risk segments.

Market risk

Compliance and operational risks

Cybersecurity and artificial intelligence

- AI as a Threat: AI lowers the barrier to entry for cybercriminals, enabling automated reconnaissance, targeted social engineering, and adaptive malware that evades traditional defenses.

- AI as a Defense: Banks are deploying AI tools to assist with threat monitoring and risk management. The OCC emphasizes that a sound understanding of these tools’ risks and benefits is essential for management.

Fraud risk

Compliance and BSA/AML

- Supervisory Tailoring: The OCC is working to reduce the regulatory burden on community banks, recently clarifying examination procedures for low-risk institutions and discontinuing the Money Laundering Risk system data collection.

- Regulatory Changes: A proposed rule is currently under consideration to amend requirements for risk-based AML and countering the financing of terrorism (CFT) programs.

Innovation and digital assets

Artificial intelligence implementation

- Governance: The OCC advocates for “human-in-the-loop” accountability.

- Challenges: Industry-wide challenges include a lack of explainability, data privacy, “data poisoning,” and validation difficulties.

- Guidance: OCC Bulletin 2026-13 recently updated model risk management guidance, though generative AI models currently fall outside its specific scope. An interagency Request for Information (RFI) on bank use of AI is expected in the near future.

Digital assets and stablecoins

- Stablecoins: The OCC issued a notice of proposed rulemaking in February 2026 to establish a federal regulatory framework for payment stablecoins.

- Tokenization: Interagency FAQs released in March 2026 clarified that the technologies used to transact in a security do not generally change its regulatory capital treatment.

OCC’s Spring 2026 Semiannual Risk Perspective and outlook for the banking industry

The banking industry enters 2026 with strong capital levels, high liquidity, and improving profitability. However, regulators increasingly warn that the speed of emerging risks may challenge traditional oversight models. Commercial real estate refinancing pressure, private credit deterioration, AI-driven cyber threats, stablecoin regulation, and geopolitical instability are reshaping the banking landscape.

As financial institutions move deeper into 2026, banks that strengthen risk management, improve operational resilience, and adapt quickly to changing market conditions will likely remain best positioned for long-term stability and growth.

By

By